Actual rate - Standard rate x Actual hours worked Labor rate variance. How to Calculate the Labor Efficiency Variance.

Compute And Evaluate Labor Variances Principles Of Accounting Volume 2 Managerial Accounting

Actual rate per hour.

. Direct labor is a cost associated with workers working directly in the production process. Direct labor rate variance AR x AH - SR x AH 1450 x 386 - 1400. The variance is unfavorable because labor worked 50 hours more than what was allowed by standard.

The formula for direct labor may be derived as. Actual total labor costs 4020000. Calculate the number of active hours Active Hours 6500 hours Step 1 - 800 idle hours 5700 hours.

1 actual labor hours actual wage rateand. Direct labor efficiency variance AH SR SH SR 12025 11700 325 unfavorable. Alternatively the variance can be calculated by using factored formula as follows.

Direct Labor Rate Variance Formula - 8 images - total direct labor cost formula. See the answer Show transcribed image text Expert Answer 100 2 ratings 1. Total labor variance Rate variance Time variance textrmTotal labor variance Rate variance Time variance Total labor variance Rate variance Time variance Total labor variance 30 500 U n f a v o r a b l e 5 500 U n f a v o r a b l e textrmTotal labor variance rm 30500 rmUnfavorable rm 5500rmUnfavorable Total.

For example assume that employees work 40 hours per week earning 13 per hour. The direct labor efficiency variance may be computed either in hours or in dollars. Calculate the direct labor hourly rate The hourly rate is obtained by dividing the value of fringe benefits and payroll taxes by the number of hours worked in the specific payroll period.

Actual hours - Standard hours x Standard rate Labor. Standard rate per hour. Direct labor quantity variance SR x SH AH.

The variance is obtained by calculating the difference between the direct labor standard cost per unit and the actual direct labor cost per unit. Actual and budgeted fixed overhead 1029600. Direct labor efficiency variance Actual labor hours budgeted labor hours.

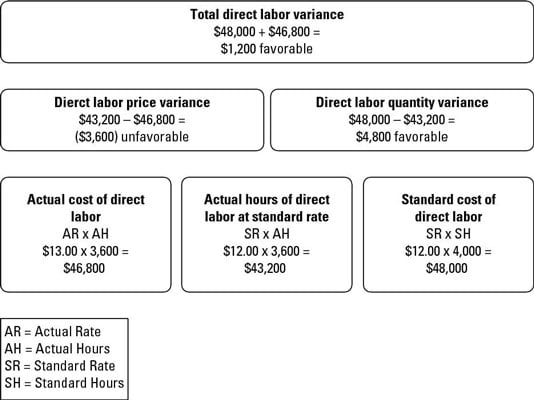

This variance is calculated as the difference between the actual labor hours used to produce an item and the standard amount that should have been used multiplied by the standard labor rate. Direct labor price variance SR AR x AH To get the direct labor quantity variance also known as the direct labor efficiency variance multiply the standard rate SR by the difference between total standard hours SH and the actual hours worked AH. In addition to evaluating materials usage companies must assess how efficiently and effectively they are using labor in the production of their products.

Calculate the total number of hours Total Hours 10000 units x 065 hours per unit 65000 hours. The labor rate variance is the difference between. An unfavorable variance means that the cost of labor was more expensive than anticipated while a favorable.

The formula for the labor efficiency variance is. How to Calculate Direct Labor Rate Variance. The company must look at both the quantity of hours used.

It is calculated as the difference between the actual labor rate paid and the standard rate multiplied by the number of actual hours worked. Previous A repeated-measures study uses a sample of n 10 participants to evaluate the mean differences among four treatment conditionsIn the analysis of variance for this study what is the. This video shows how to calculate the labor rate variance.

About Press Copyright Contact us Creators Advertise Developers Terms Privacy Policy Safety How YouTube works Test new features Press Copyright Contact us Creators. The number of hours actually worked during a particular period of. It is the actual hourly rate paid to labor.

View the full answer. Inputs to be provided. Suppose for example the standard time to manufacture a product is one hour but the product is completed in 115 hours the variance is 015 hours unfavorable.

The following example will help you to understand further. A 236250 favorable. Actual variable overhead costs 4520000.

Direct labor efficiency variance SR AH SH. The direct labor time variance is. The direct labor variance is the difference between the actual labor hours used for actual production and standard labor hours allowed for actual production on standard labor hour rate.

This problem has been solved. B Labor Efficiency Variance. If the actual direct labor cost per unit is higher than the standard direct labor cost per unit it means that the company incurs more to produce one unit of a product than is expected making the cost unfavorable to the business.

From the definition you can easily derive the formula. Overhead is applied on standard labor hours. Standard variable overhead rate 2450 per standard labor hour.

Employing diagrams to work out direct labor variances. It is the hourly rate determined at the time of setting standards. How to used direct labor rate variance calculator.

Standard rate actual hours used Actual rate Actual Hours used So Actual Hours Used Actual Rate Standard Rate Direct Labor Rate Variance. Compute and Evaluate Labor Variances.

Compute And Evaluate Labor Variances Principles Of Accounting Volume 2 Managerial Accounting

How To Calculate Direct Labor Variances Dummies

Compute And Evaluate Labor Variances Principles Of Accounting Volume 2 Managerial Accounting

0 Comments